Filing for bankruptcy is one of the hardest financial decisions you'll ever make—but often, it's also the best. Chapter 7 bankruptcy (often called "liquidation") is designed to wipe the slate clean, eliminating unsecured debts like credit cards, medical bills, and personal loans in as little as 90 days.

But what does the process actually look like? This guide walks you through every step of the timeline, so you know exactly what to expect. If you are still comparing Chapter 7 against a repayment plan, start with our consumer bankruptcy overview and then review Chapter 13 guidance before you decide.

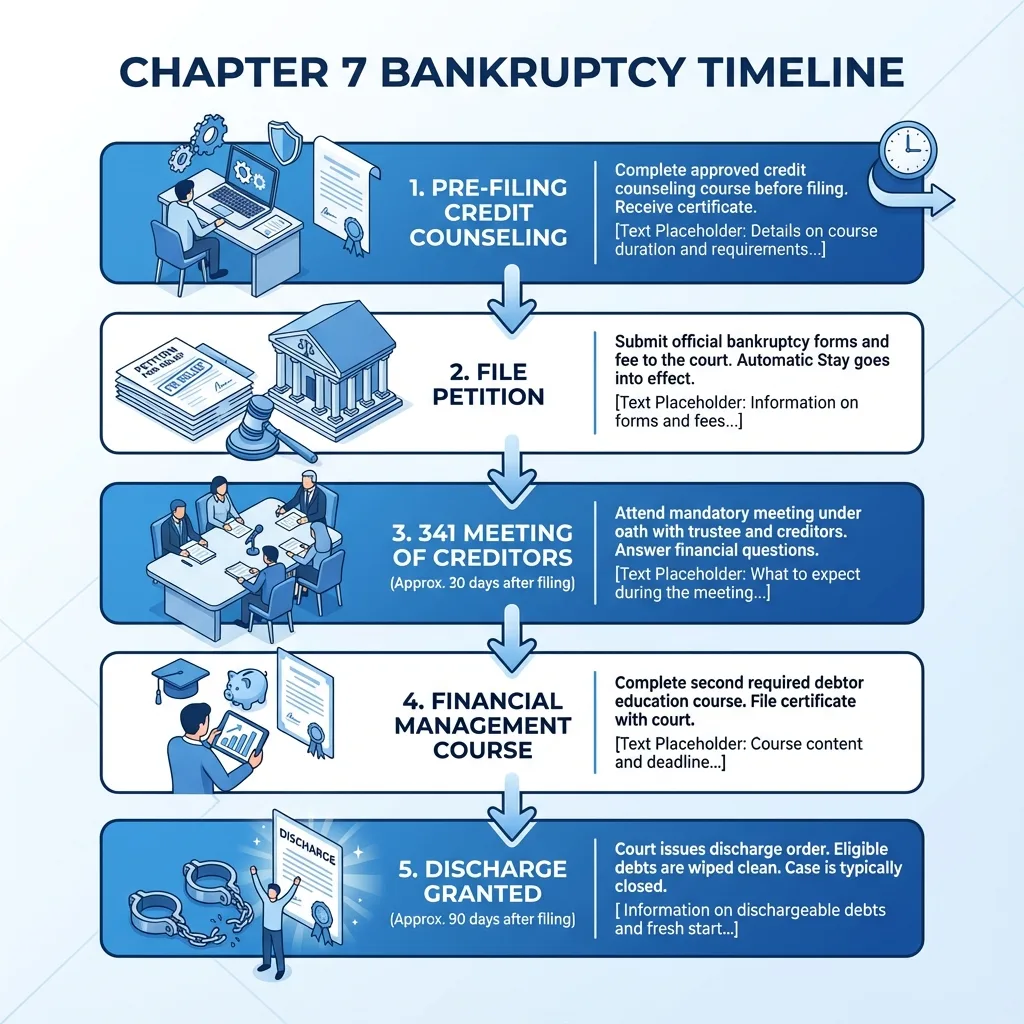

The Chapter 7 Timeline

Step 0: Pre-Filing Requirements

Before you can file anything, the law requires you to complete a Credit Counseling Course from an approved provider. This usually:

- Takes about 60-90 minutes online or over the phone

- Costs $10 to $50 (waivers available for low income)

- Must be completed within 180 days before filing

Step 1: Filing the Petition

Your attorney will file your "Voluntary Petition" with the bankruptcy court. This massive packet includes:

- Schedule A/B: All your property (house, car, clothes, bank accounts)

- Schedule D/E/F: All your debts (secured, priority, unsecured)

- Form 122A-2: The "Means Test" calculation to prove you qualify

⚡ The Automatic Stay

The moment your petition is filed, an Automatic Stay goes into effect. This is a federal court order that immediately stops all collection activity, including lawsuits, garnishments, and phone calls.

Step 2: The 341 Meeting of Creditors

About 30 to 40 days after filing, you will attend a meeting with the Bankruptcy Trustee (usually via Zoom or phone these days).

What happens:

- You are placed under oath

- The Trustee asks basic questions: "Did you list all your assets?" "Did you list all your debts?"

- Creditors can attend, but usually don't

Most meetings last less than 10 minutes.

Step 3: The Discharge

After the meeting, you have one final task: The Debtor Education Course (Financial Management Course). Like the first course, it takes about 2 hours.

Approximately 60 days after your 341 meeting, providing no creditors objected, the court issues your Discharge Order.

🎉 What This Means:

- Your legal obligation to pay discharged debts is gone forever

- Creditors can never contact you about these debts again

- You can start rebuilding your credit immediately

What Debts Are Erased?

✅ Discharged (Erased)

- Credit Card Debt

- Medical Bills

- Personal Loans

- Payday Loans

- Utility Bills (past due)

- Repossession Deficiencies

❌ Not Discharged (Usually)

- Student Loans (unless undue hardship)

- Child Support & Alimony

- Recent Income Taxes (less than 3 years old)

- Court Fines & Restitution

- Debts from Fraud

Is Chapter 7 Right For You?

Chapter 7 is a powerful tool, but it's not for everyone. You must pass the "Means Test" (earn below the state median income) and be willing to potentially part with non-exempt luxury assets (though most clients keep everything they own thanks to exemptions).

Don't guess at your eligibility. A simple consultation can tell you exactly what you can keep and what you can wipe out.