People searching for the Chapter 7 process usually want one thing: a straight answer about what happens next. Not a slogan. A timeline.

That is what this article is for. It walks through the ordinary sequence in a consumer Chapter 7 case: what has to happen before filing, what the filing triggers immediately, when the 341 meeting of creditors usually occurs, what has to be completed before discharge, and why some cases stay open longer than others.

If you are still deciding whether Chapter 7 is even the right chapter, start with our consumer bankruptcy overview and then compare it against our Chapter 13 guide. This article assumes you are focused on the process itself.

Before You File: Eligibility, Documents, and Credit Counseling

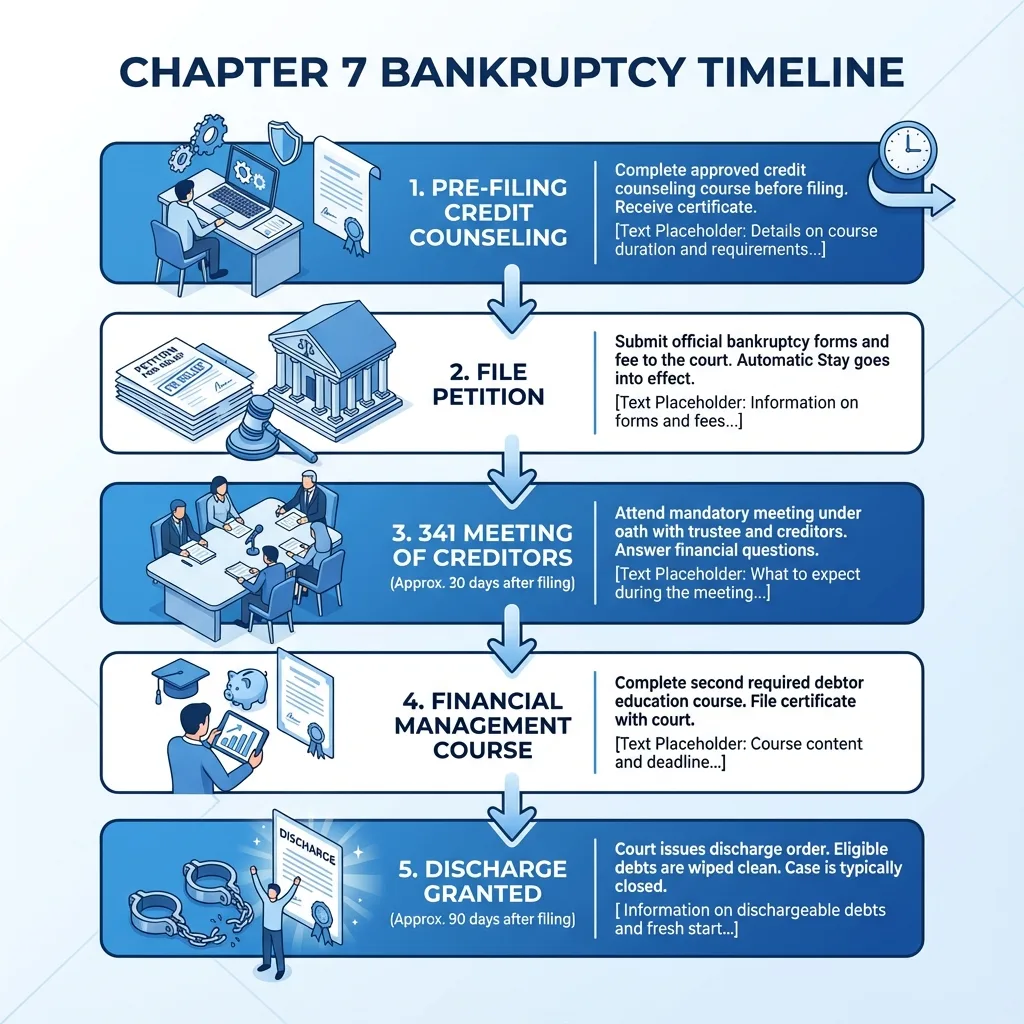

A Chapter 7 case starts before the petition is filed. Individual debtors generally must complete an approved credit-counseling briefing within the 180 days before filing. If that requirement is missed, eligibility itself can become a problem.

This is also the stage where the real file is built. A lawyer will usually need pay information, tax returns, bank statements, a list of assets, a list of debts, and enough detail to analyze exemptions and Chapter 7 eligibility. In many cases, the means test and exemption analysis are the work that determines whether Chapter 7 is the right tool or whether a Chapter 13 repayment plan is safer.

If you want the chapter-specific legal overview after reading this timeline, review our Chapter 7 bankruptcy attorney page for the qualification and discharge side of the analysis.

Filing Day: The Petition Goes In and the Automatic Stay Starts

Once the petition, schedules, and related forms are filed, the case formally begins. That filing triggers the automatic stay in most situations. In plain English, the automatic stay is the federal court order that generally stops collection activity from moving forward against the debtor right away.

The stay can affect collection calls, lawsuits, garnishments, and other efforts to collect pre-petition debts. It is powerful, but it is not magic. Some issues require follow-up with the court, the trustee, or creditors, and some obligations have different treatment under the Bankruptcy Code.

Filing day is also when the court appoints a Chapter 7 trustee and the case starts moving on its own deadlines. That is why accuracy matters so much. A rushed or incomplete filing can create avoidable problems later in the case.

The First Few Weeks After Filing

After filing, the court sends notice of the case and schedules the meeting of creditors. In an ordinary consumer case, that meeting is usually set about a month after filing, although the exact date can vary by court and case administration.

During this period, the trustee may request supporting documents, and the debtor may need to provide tax returns, identification, pay information, or other records. If secured property is involved, the debtor may also need to decide whether to surrender it, redeem it, or enter into a reaffirmation agreement.

This is the phase where many people expect drama and instead get paperwork. That is normal. Chapter 7 is often document-heavy and short on courtroom theatrics.

The 341 Meeting of Creditors

The 341 meeting is one of the most searched parts of the process because the name sounds more intimidating than the event usually is. In a typical consumer case, it is a short meeting with the trustee, not a full-blown trial in front of a judge.

The debtor is placed under oath and asked questions about the petition, schedules, assets, debts, transfers, and general financial affairs. The goal is to confirm that the papers are accurate and complete. Creditors are allowed to appear, but in many routine consumer cases they do not.

Most people are asked straightforward questions: Did you review the petition before signing? Did you list all assets and debts? Have you transferred anything recently? Do you expect an inheritance or claim? The meeting is important, but for many debtors it is brief and procedural.

After the 341 Meeting: Debtor Education and Waiting for Discharge

There is still work left after the 341 meeting. An individual debtor must complete an approved debtor-education or financial-management course before discharge can be entered. Missing that step can delay or prevent discharge even when the rest of the case went smoothly.

If nobody files a timely objection to discharge and there are no major unresolved issues, the court usually enters the discharge order relatively early in the case. The U.S. Courts explains that, in most Chapter 7 cases, discharge is generally issued 60 to 90 days after the date first set for the meeting of creditors.

That is why people often describe Chapter 7 as a four-to-six-month process from filing to discharge in an ordinary no-asset case. It can be faster than consumers expect, but it is still built on deadlines and required steps.

Why a Chapter 7 Case Can Stay Open Longer

A discharge does not always mean the case is fully closed the same day. A case can remain open while the trustee finishes administration, especially if there are nonexempt assets to liquidate, unresolved exemptions, turnover issues, tax matters, or other estate-administration work.

That distinction matters because consumers often use discharge and case closing interchangeably. They are related, but they are not the same event. You can receive a discharge and still see the case remain open while administrative issues are wrapped up.

What Chapter 7 Usually Does - and Does Not - Wipe Out

Chapter 7 is often used to discharge unsecured debts such as credit cards, medical bills, personal loans, and deficiency balances. But not every debt disappears. Student loans, domestic-support obligations, many recent taxes, criminal fines, and debts tied to certain misconduct can be treated differently. If your Chapter 7 question comes from a divorce decree assigning joint debts to your ex, read our guide to Chapter 7 and divorce debt before assuming family-court enforcement is the only path.

That is why the timeline is only part of the analysis. A fast case is useful only if the chapter actually solves the debt problem you have. If the main issue is arrears on a house or car that you want to keep, the comparison with Chapter 13 bankruptcy becomes more important than the speed of Chapter 7.

Need The Qualification Analysis, Not Just the Timeline?

If you are beyond the research stage and need to know whether Chapter 7 fits your income, assets, and goals, review our Chapter 7 attorney page for the eligibility and discharge issues this timeline does not answer by itself.

A Practical Chapter 7 Checklist

- Complete approved credit counseling within the 180-day window before filing.

- Gather income, tax, bank, debt, and asset records.

- File the petition and schedules accurately.

- Use the automatic stay period to stabilize the case and respond to trustee requests.

- Attend the 341 meeting and answer questions truthfully.

- Complete debtor education before discharge is due.

- Track whether the case is only discharged or actually fully closed.

That is the real shape of a normal Chapter 7 case. The exact dates move, but the sequence does not.

This article is for educational purposes only and does not create an attorney-client relationship. Chapter 7 eligibility, exemption planning, and discharge issues depend on individual facts and local procedure. Last updated: April 2026.