When a debt collector crosses the line, the case usually turns on one question: what did you save? That is why FDCPA record keeping matters so much. A collector may deny the call pattern, deny the text message, or say the letter said something different. Your evidence is what closes that gap.

The goal is not to turn every consumer into a forensic investigator. The goal is simpler: keep the records that show who contacted you, when they did it, what they said, and what happened after you responded.

This article is built for that practical job. It covers the evidence most worth saving, where people accidentally lose good proof, and how to preserve a file that is usable if you later need an FDCPA attorney.

Why Evidence Matters So Much in FDCPA Cases

The Fair Debt Collection Practices Act regulates what third-party debt collectors can say and do. But a rights page by itself does not prove a violation. The proof usually comes from ordinary records: screenshots, letters, envelopes, call logs, voicemails, dispute letters, certified-mail receipts, and credit-report snapshots.

That is especially important now because debt collection does not happen only by phone. A modern case file may include text messages, emails, portal notices, and credit-report furnishing. If you are already disputing the debt, pair this article with our debt validation letter guide so you preserve the dispute itself correctly.

Collectors also have their own record-retention duties under Regulation F. But do not assume their records will be complete, easy to obtain, or preserved in the way you need. Build your own file from day one.

Start With a Simple Master Timeline

The first document to create is a basic timeline. It can be a notes app, spreadsheet, or paper log. What matters is that you use one place consistently.

- Date and time: note when the contact happened.

- Channel: phone call, voicemail, text, email, letter, portal message, lawsuit paper, or credit-report entry.

- Number or sender: capture the phone number, email address, short code, collector name, or law firm name.

- What was said: write a short summary while it is fresh.

- Your response: note if you disputed the debt, asked them to stop, or sent a letter.

This timeline keeps the file usable. Without it, people often have good evidence scattered across a phone, inbox, and kitchen drawer but no clear story tying it together.

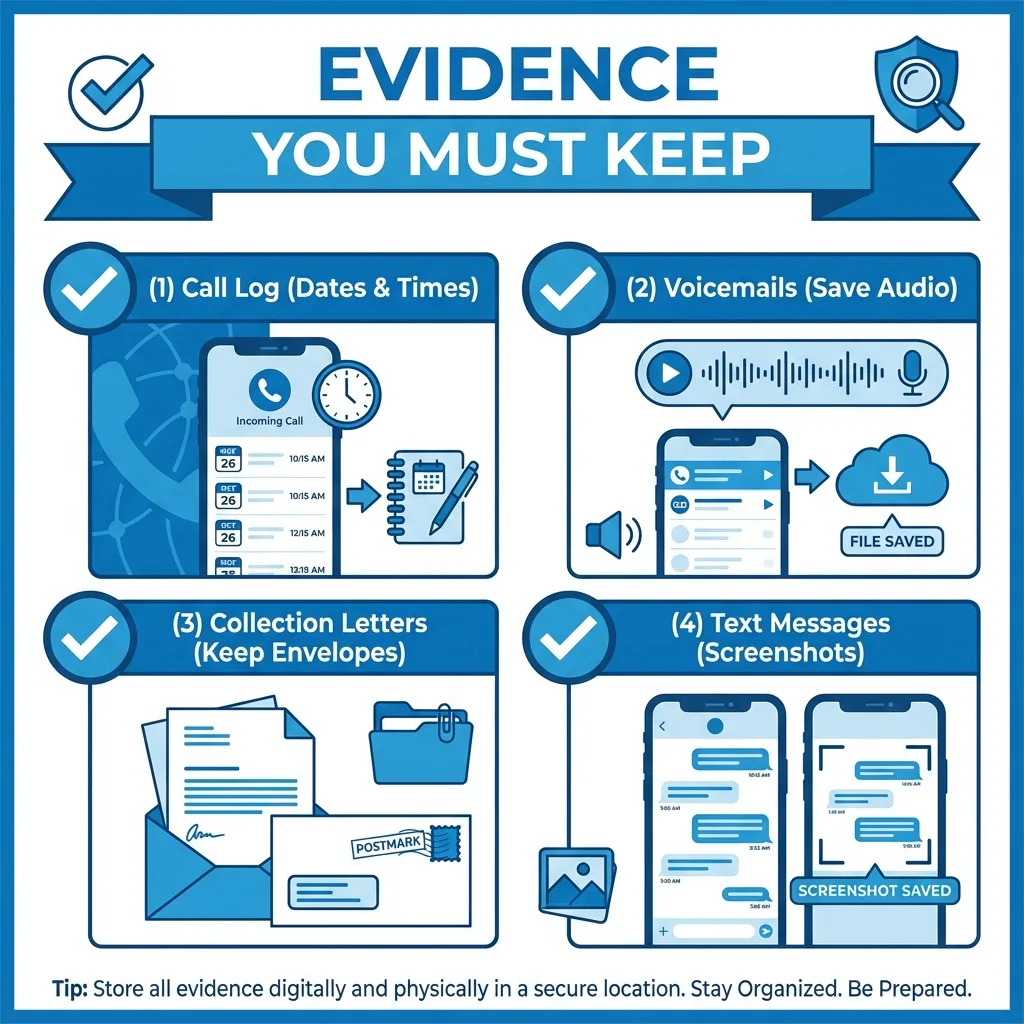

Save Every Letter - Including the Envelope

Physical mail still matters. Save the letter itself, any inserts, and the envelope. The envelope can show the postmark and helps you prove when the collector actually sent the notice.

That can matter when timing is part of the claim. If you are analyzing whether the collector gave the right validation notice, whether a dispute was timely, or whether a later letter contradicted an earlier one, the mailing date becomes part of the proof.

Scan or photograph each page and save the file with a name that makes sense later, such as 2026-04-17-collector-letter-page-1.pdf. Do not rely on your camera roll to stay organized on its own.

Preserve Text Messages, Emails, and Portal Messages Correctly

For digital communications, screenshots are only the start. You should also save the full thread when you can.

- Text messages: capture the phone number, date, time, and the full thread, not just the most offensive line.

- Emails: save the full message as a PDF or print it to PDF so you preserve the sender, date, and subject line.

- Portal messages: if the collector forces you into a portal, save screenshots of the login page, the message, and any deadlines or payment prompts.

Collectors that use digital channels still have to follow the FDCPA and Regulation F. If the message contains a misleading demand, keeps going after an opt-out, or conflicts with a written dispute, you want the full message trail intact. For a broader look at stopping digital contact, see our guide on responding to debt collector texts and emails.

Calls and Voicemails: What To Capture

Calls are where many consumers lose useful evidence because they rely on memory. Save the call log itself and write down what happened. If the collector left a voicemail, preserve it immediately.

- Call logs: screenshot the incoming and outgoing call history.

- Voicemails: save the audio file if your phone allows it, or back it up by forwarding it or recording a clean copy to secure storage.

- Notes: write down the caller's name, company, what they demanded, and whether they threatened a lawsuit, arrest, garnishment, or employer contact.

If you are considering recording a live call, stop and check your state's consent rules first. Those laws vary. If you are not sure, call logs and voicemails are still strong evidence, and they avoid creating a separate consent issue.

Do Not Forget Credit Reports and Dispute Records

Many FDCPA matters overlap with credit reporting. If the collector reported the account, save snapshots of the tradeline before and after a dispute. Pull your reports through AnnualCreditReport.com and save the relevant pages as PDFs.

If you disputed the debt, save:

- the dispute letter or email you sent,

- certified-mail receipts or delivery confirmation,

- the green card or electronic proof of delivery, and

- any response from the collector.

That documentation often matters as much as the collector's original message. A file with a clean dispute trail is much stronger than a file that only shows the consumer was upset.

How Long Should You Keep Debt Collection Records?

As a practical rule, keep the file until the matter is fully resolved and then keep it longer than feels convenient. Regulation F requires debt collectors to retain records that show compliance or noncompliance, generally for three years after their last collection activity on the debt, and recorded calls for three years after the date of the call if they record them.

Consumers should think in similar terms. Do not throw away records just because the calls stopped for a month. Old debts get sold, new agencies appear, and a quiet period is not the same thing as a resolved matter.

Also remember that FDCPA claims have their own filing deadlines. If you think you may have a claim, do not wait for perfect record keeping before talking to counsel. Save what you have and get legal guidance promptly.

Preserve the File Before It Gets Worse

If the collector is still contacting you, save today's evidence before you decide what to do next. Then compare your options in our cease and desist letter guide and our step-by-step harassment guide.

Best Practices for Backups and File Names

Good evidence can still become useless if it is buried or lost. Use one folder for the matter. Create subfolders for letters, screenshots, call logs, audio, disputes, and credit reports. Name files with the date first so they sort chronologically.

If possible, keep a second backup outside your phone. Emailing files to yourself is better than nothing, but a secure cloud folder or external drive is usually cleaner.

The point is not perfection. The point is being able to put your hands on the file six months from now and understand it in ten minutes.

The Evidence Checklist To Prioritize First

- Your master timeline.

- Every collection letter and envelope.

- Screenshots of texts, emails, and portal messages.

- Call-log screenshots and saved voicemails.

- Certified-mail proof for disputes or stop-contact letters.

- Credit-report snapshots if the account was furnished.

If you build those six categories early, you will usually have enough to reconstruct the problem and evaluate whether the collector violated the law.

This article is for educational purposes only and does not create an attorney-client relationship. Evidence issues can overlap with state recording laws, credit reporting disputes, and court deadlines. Last updated: April 2026.