If debt collectors are harassing you with constant calls, threats, or misleading statements, you have legal protections under the Fair Debt Collection Practices Act (FDCPA). But navigating these laws alone can be overwhelming. That's where an experienced FDCPA attorney comes in.

This guide will help you find the right legal representation to protect your rights and hold abusive debt collectors accountable.

What Does an FDCPA Attorney Actually Do?

An FDCPA attorney specializes in protecting consumers from illegal debt collection practices. Here's what they can do for you:

📋 Case Evaluation

Review your situation, communications, and documents to identify FDCPA violations.

🛡️ Stop the Harassment

Send cease communications letters and ensure collectors follow the law.

⚖️ Legal Action

File lawsuits against violators and pursue statutory damages up to $1,000 per lawsuit.

💰 Recover Damages

Seek compensation for emotional distress, lost wages, and attorney's fees.

"Once a debt collector knows you have an attorney, they must communicate through your lawyer—giving you immediate relief from harassing calls."

When Should You Hire an FDCPA Attorney?

Not every annoying call is a lawsuit. But debt collection crosses into illegal territory more often than people realize, and the Fair Debt Collection Practices Act (FDCPA), 15 U.S.C. § 1692, spells out exactly when. It is time to call an attorney if a collector has:

- Called repeatedly to harass or intimidate you, or used threats or obscene language — barred by 15 U.S.C. § 1692d

- Lied about the amount, posed as a lawyer or government agent, or threatened arrest or garnishment they can't deliver — barred by 15 U.S.C. § 1692e

- Added unauthorized fees or used other unfair tactics — barred by 15 U.S.C. § 1692f

- Called before 8 a.m. or after 9 p.m., contacted you at work after you said stop, or told your family or coworkers about the debt — barred by 15 U.S.C. § 1692c

One detail tilts these cases in your favor. Courts do not measure a collector's conduct against a careful, savvy reader. Most apply the "least sophisticated consumer" standard — the Seventh Circuit calls its version the "unsophisticated consumer" standard — asking whether the communication would mislead an unsophisticated person, not whether it fooled you. If a letter or call clears that low bar for deception, the violation stands. For the full rundown of banned tactics, see our guide to the Fair Debt Collection Practices Act.

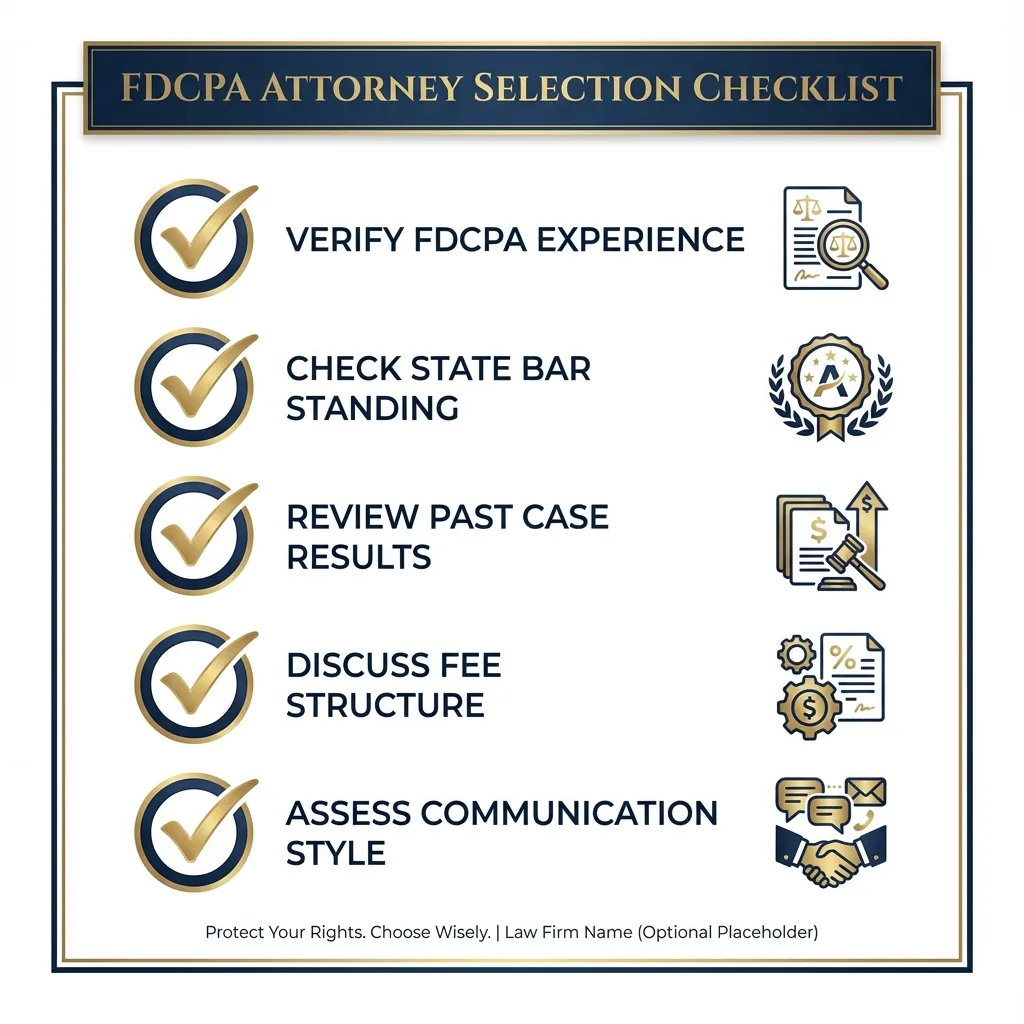

5 Essential Qualifications to Look For

1. Specific FDCPA Experience

Consumer law is a specialized field. You want an attorney who has handled dozens or hundreds of FDCPA cases—not someone who dabbles in it occasionally. Ask specifically: "How many FDCPA cases have you litigated?"

2. Verified State Bar Standing

Before hiring anyone, verify their license through your state bar association. This confirms they're in good standing and haven't faced disciplinary action.

3. Proven Track Record

Ask about their case results. A good FDCPA attorney should be able to share examples of settlements and verdicts they've achieved for clients in similar situations.

4. Clear Fee Structure

Most FDCPA attorneys work on contingency—meaning you pay nothing upfront and they only get paid if you win. The FDCPA also allows winning plaintiffs to recover attorney's fees from the defendant.

5. Strong Communication

Your attorney should be responsive and keep you informed. During your consultation, notice how well they listen and explain things in plain language.

Questions to Ask During Your Consultation

A free consultation is your chance to evaluate the attorney. Here are the essential questions:

| Question | What You're Looking For |

|---|---|

| "How many FDCPA cases have you handled?" | At least 50+ cases, ideally 100+ |

| "What's your strategy for my case?" | Clear, specific plan tailored to your situation |

| "How do your fees work?" | Contingency with no upfront costs |

| "Can you share similar case results?" | Specific examples with dollar amounts |

| "How will we communicate?" | Clear expectations for response times |

How FDCPA Attorney Fees Actually Work

The biggest myth about suing a debt collector is that you can't afford to. You can. The FDCPA was built so the people it protects don't pay out of pocket to enforce it.

Almost every reputable FDCPA attorney works on contingency: no retainer, no hourly bills, and no fee at all unless you win. On top of that, the statute makes the collector who broke the law pay your attorney's fees and costs under 15 U.S.C. § 1692k(a)(3). So when you recover statutory damages of up to $1,000 under 15 U.S.C. § 1692k(a)(2)(A) — plus any actual damages — that money goes to you, not to legal bills.

Before you sign, confirm three things: that the fee is contingent, that you owe nothing if the case loses, and who fronts court costs along the way. A trustworthy lawyer puts all of it in writing. Results vary, and no attorney can promise a specific outcome.

Local Lawyer or National Firm?

The FDCPA is a federal law, so you are not limited to an attorney down the street. A firm that handles debt collection cases across the country often brings far more FDCPA-specific reps than a local generalist who takes one of these cases a year. What matters is depth in this statute, not proximity.

State law is the one place geography counts. Many states layer their own protections on top of the FDCPA — and some reach original creditors the federal law doesn't. The right attorney checks whether your state's consumer protection laws add claims worth pursuing, then handles the federal and state pieces together.

🚩 Red Flags to Avoid

Not every attorney advertising FDCPA services is equally qualified. Watch out for these warning signs:

Ready to Take Action?

If debt collectors are violating your rights, don't wait. The FDCPA has a one-year statute of limitations, so time is critical.

This guide explains how to choose an FDCPA attorney in general terms and is not legal advice. The Fair Debt Collection Practices Act has a one-year statute of limitations (15 U.S.C. § 1692k(d)), so if you believe a collector violated your rights, speak with a licensed attorney promptly.