A credit score is a number lenders and other decision-makers use to estimate risk. It is not a moral judgment, and it is not the whole story of your finances. But it can affect whether you get approved for a mortgage, auto loan, credit card, apartment, or other financial product - and what rate or terms you get if you are approved.

That makes the question what a credit score is a fair one, especially because consumers rarely have just one score. They may see a FICO Score, a VantageScore, or multiple versions of each depending on who pulled the report and when.

This guide explains the basics without pretending every score works the same way. It also covers the part many generic explainers miss: when a low score is not just a budgeting problem, but a sign of inaccurate reporting, fraud, or identity theft.

What a Credit Score Measures

A credit score is designed to predict how likely a borrower is to repay credit obligations. In other words, it is a risk model built from the information in a consumer's credit report. The better the report data looks from the model's perspective, the stronger the score tends to be.

That also means the score is only as reliable as the underlying report. If the report contains the wrong balance, the wrong account, a mixed file, or a fraudulent tradeline, the score can move in the wrong direction for the wrong reason.

If your current concern is not the definition of a credit score but whether a bureau or furnisher failed to fix an error, start with our guide to disputing inaccurate credit reports.

FICO vs. VantageScore

The two names most consumers see are FICO and VantageScore. They are both credit-scoring models, but they are not identical. That is why two legitimate scores pulled close together can still be different.

FICO says its scores are used by 90% of top lenders, and its standard base score range is generally 300 to 850. VantageScore also uses a 300 to 850 range in its modern consumer-facing models, but it applies its own model logic and can score some consumers differently based on the data available at the bureau that generated the score.

That is why the right question is usually not which one is fake. The right question is what data was used, which model was used, and what decision is being made. If you want a deeper side-by-side explainer, read our article on VantageScore vs. FICO.

Common Credit Score Ranges

Most consumer-facing base scores use a 300 to 850 range. In FICO's standard framing, scores below 580 are poor, 580 to 669 are fair, 670 to 739 are good, 740 to 799 are very good, and 800 or above are exceptional.

Those labels are helpful for orientation, but do not treat them like universal approval rules. A lender can still deny someone with a good score because of debt-to-income issues, incomplete income documentation, or a product-specific underwriting rule. The score is powerful, but it is not the entire file.

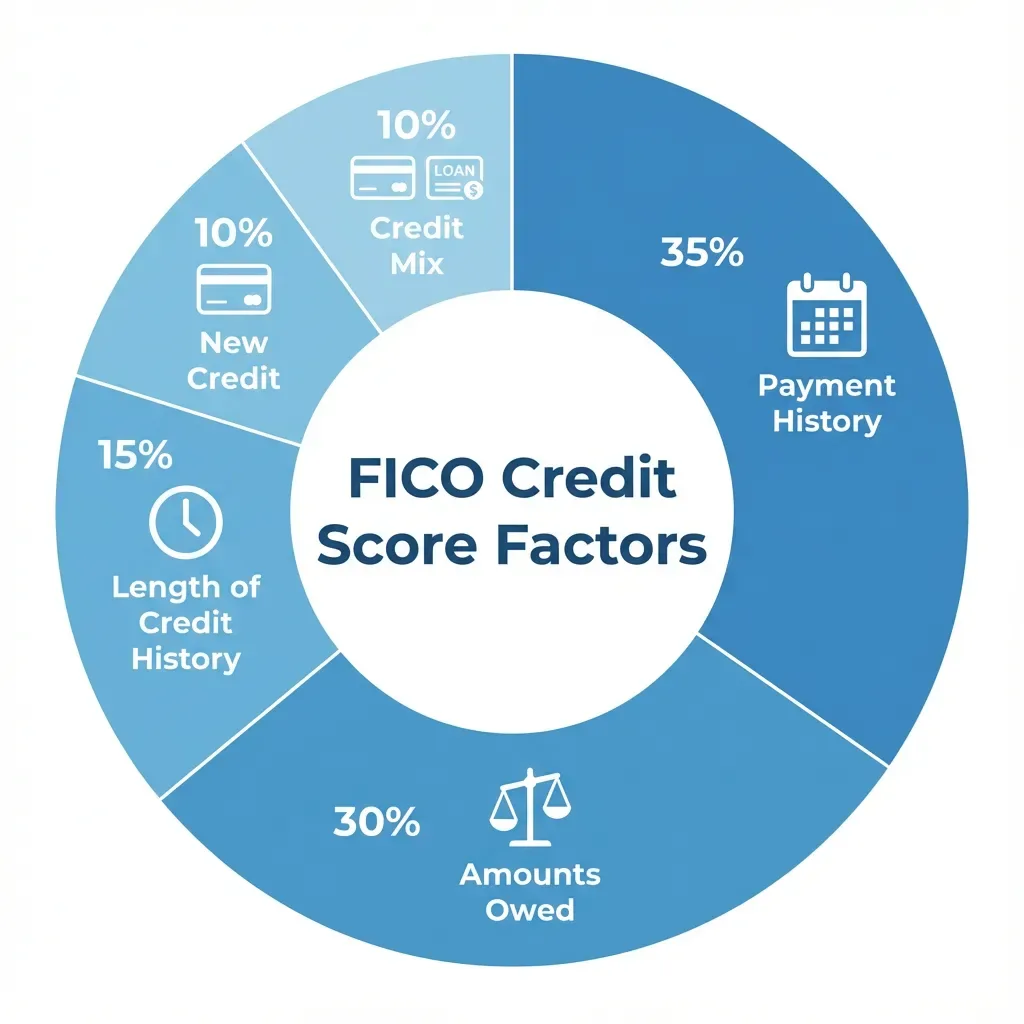

What Usually Lowers a Credit Score

For FICO, the main categories are payment history, amounts owed, length of credit history, new credit, and credit mix. Missed payments, high utilization, a short history, or a burst of recent applications can all pull the score down.

That does not mean every common myth is true. Your salary, your job title, and checking your own score are not themselves part of the standard FICO formula. A lender may care about income and employment for underwriting, but that is different from the score calculation itself.

One of the easiest misconceptions to fix is the belief that checking your own score hurts it. It does not. FICO explains that soft inquiries, such as viewing your own report or score, do not affect your FICO Scores. Hard inquiries from active applications can.

Why Scores Change From Month to Month

Credit scores move because the underlying reports move. A new balance posts. A payment reports late. A card gets paid down. An old account ages. A collection account appears. A bureau updates one file before another. That is also why your scores from different bureaus can diverge on the same day.

The takeaway is practical: if a score change surprised you, check the underlying reports before assuming the score itself is wrong. The FTC and AnnualCreditReport materials make that step easy to remember. The report comes first; the score is built on top of it.

When a Credit Score Drop Is a Legal Red Flag

Not every score drop means you need a lawyer. But some do point to legal or factual problems instead of ordinary credit use.

- A tradeline that is not yours: possible identity theft or mixed-file reporting.

- A debt that should have been corrected or removed: possible bureau or furnisher dispute failure.

- A background-screening or fraud problem that triggered a denial: possible FCRA issues beyond the score itself.

- A sudden score collapse after account fraud: check for identity-theft accounts or unauthorized use.

If that sounds familiar, our identity theft attorney page and our FCRA practice page are the right next resources rather than another generic score explainer.

How To Check the Underlying Reports for Free

Consumers can get their credit reports through AnnualCreditReport.com, the official source authorized for those reports. The FTC explains that consumers can check each nationwide bureau's report there once a week for free.

That is one of the best habits to build if your score matters in the near term. You cannot meaningfully improve or defend a credit score if you do not know what is in the file driving it.

What To Do If You Find Something Wrong

First, save the report showing the problem. Then identify whether the issue is an inaccurate account, a wrong balance, identity theft, a mixed file, or a collector reporting something that does not line up with the facts.

From there, the next step depends on the problem:

- For ordinary inaccuracies, use the dispute process with the bureau and furnisher.

- For fraudulent accounts, pair the dispute process with identity-theft recovery steps.

- For credit-repair pitches that promise to fix accurate reporting for money, step back and read our credit repair scam guide before paying anyone.

Score Drop With a Real Reporting Error?

If your score dropped because the wrong information hit your file - not because you missed payments - the legal issue is often the report, not the number. Start with our credit-report dispute guide and then review our FCRA representation page.

The Practical Answer

A credit score is a risk score built from your credit report. It matters because lenders and other decision-makers use it. But the score itself is not the whole problem and not always the real problem. Sometimes the real issue is the underlying data.

That is why smart consumers do two things at once: they manage the habits that affect scores over time, and they check the reports often enough to catch fraud or inaccurate reporting before those mistakes harden into denied loans, higher rates, or lost housing opportunities.

This article is for educational purposes only and does not create an attorney-client relationship. Credit-score issues can overlap with identity theft, mixed files, and consumer-reporting disputes. Last updated: April 2026.